文

A

In Southeast Asia game globalization, Vietnam is often seen as a market that requires deep localization. But the real challenge has never been only language translation or channel launch. It is a full set of local game industry capabilities formed by payment, communities, customer service, regulation, offline reach, and long-term operations. The reason VNG Games is hard to bypass is precisely that over the past two decades, it has participated in building almost this entire capability stack.

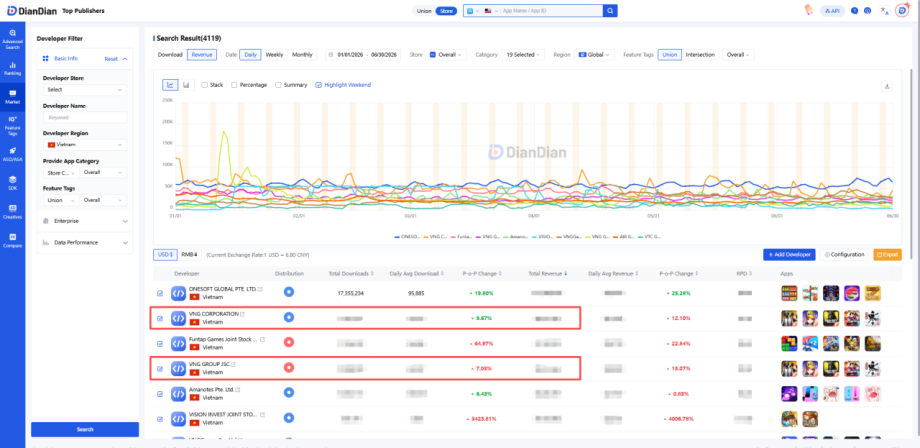

First, look at the revenue performance of Vietnam's mobile game companies: according to Diandian data,based on the metric of the first half of 2026total game-product revenue generated by Vietnam-based game companies on the App Store and Google Play,the two game-related entities within the VNG ecosystem—VNG Games and VNG—both rank near the top of the developer revenue chart. If the revenue scale of the two is combined, the VNG ecosystem's revenue performance wouldclearly widen the gap with the second-ranked company.

However,if VNG Games is understood only as a game publisher, it is easy to underestimate its real position in Vietnam's game market.

It certainly does publishing, and it has long relied on licensed third-party products to contribute revenue. But more importantly, over the past two decades, VNG's game business has participated in building almost the entire local infrastructure required for monetizing online games in Vietnam.

This infrastructure includes server deployment, top-up and payment, internet cafes and channels, player communities, customer-service systems, as well as offline events, localized operations, and compliance communication.

This is also why VNG Games is often unavoidable when discussing Vietnam's game industry. It is not simply an intermediary that brings a game into the market, but more like one of the foundation companies of Vietnam's game industry: on one hand, it connects overseas game content with local players; on the other, it turns payment, communities, customer service, event operations, and long-term service capabilities into a reusable local publishing system.

The scope needs to be clarified first. VNG Games, as discussed in this article, is not an independently listed financial entity, but an important part of the Games & Entertainment / Online Games business under the VNG Corporation / VNG Ltd system. Therefore, when this article discusses revenue, gross bookings, and user data, it refers to game-related businesses under VNG Group's disclosed reporting scope, rather than the standalone financial statements of a separate company.

According to the latest disclosures, this business remains the most important revenue pillar of VNG Group. According to VNG's 2025 annual report, revenue from Games & Entertainment reached VND 7,054 billion (approximately RMB 1.83 billion), up 8% year-on-year; gross bookings (a non-GAAP operating metric used by VNG to evaluate game-segment performance, reflecting users' cash spending during the corresponding period and not equivalent to financial-statement revenue) reached VND 8,162 billion (approximately RMB 2.109 billion), up 13% year-on-year. In the same year, Games & Entertainment accounted for about 65% of VNG Group's revenue.

Looking further back, VNG once disclosed in its F-1 (a U.S. Securities and Exchange Commission registration statement used to disclose the business, financials, and risks of a company planning to list in the U.S.) that the Games business contributed 80.0% of total revenue in 2022 and 81.7% in the first half of 2023. The proportion varies across years and disclosure scopes, but what can be confirmed is that the game business has long been the core segment of VNG's commercial system.

1. Start with the group structure: VNG Games is not an isolated game brand

When discussing VNG Games, it is easy to focus only on which games it has published. But when placed back into the VNG Corporation / VNG Ltd group system, VNG Games is more like a set of business capabilities within the group's digital ecosystem responsible for game publishing, operations, content exploration, and player services.

This is also why this article repeatedly emphasizes reporting scope: VNG Games is not an independently listed entity with standalone financial statements, but a business brand and business collection under VNG's Games & Entertainment / Online Games segment. Its relationship with Zalo, ZaloPay, cloud, AI, and other businesses within the group is more about potential synergy and capability complementarity, rather than a simple equity-control relationship or direct revenue source.

If summarized in one diagram, it can be understood through the following "business architecture tree":

This structure illustrates one feature of VNG Games: it is not isolated in game agency operations, but is backed by a full set of local digital-service capabilities. Zalo can provide user reach, community, and customer-service foundations; ZaloPay corresponds to local payment understanding; and cloud and AI businesses are related to later R&D efficiency, operations automation, and platform capabilities.

These capabilities should not be directly equated with game revenue growth, but together they reduce the friction VNG faces in conducting long-term operations in Vietnam.

2. VNG Games did not start with just licensing one game

The starting point of VNG's game business can be traced back to 2004.

At that time, Vietnam's game market was still in its early stage. For a game company, the challenge was not just finding a product, securing a license, and completing launch. More fundamental questions included: how to keep servers running stably, how players could top up, how to cover internet-cafe channels, how to maintain communities, how customer service should respond, and how to organize offline promotion and player events.

In mature markets, these links are already shared by platforms, payments, channels, and service providers. But in Vietnam at the time, companies often had to build them layer by layer on their own.

Public reports show that as early as November 2004, VinaGame signed with Kingsoft to publish Võ Lâm Truyền Kỳ. Around 2005, this product became a key milestone in the development of its game business.

For Chinese readers, Võ Lâm Truyền Kỳ can be understood as the localized Vietnamese version of Kingsoft's JX Online-related product. Compared with a simple sense of "successful licensing," the more important value of this product was that it validated a localized publishing business system aimed at Vietnamese players.

This system included content translation and cultural adaptation, as well as top-up and prepaid-card systems, offline internet-cafe reach, player community operations, customer support, and an event cadence built around long-lifecycle products.

In other words, Võ Lâm Truyền Kỳ did not merely contribute a representative game; it helped VNG establish an early methodology for "how to operate online games in Vietnam."

This also explains why VNG Games was later able to continuously take on different types of overseas products. Publishing capability is not reflected only in launch efficiency, but also in understanding local player behavior, spending habits, community culture, and operating cadence.

For a regional market like Vietnam, this type of capability is especially important. When overseas publishers enter the market, they often face multiple issues around language, payments, channels, regulation, player communication, and content acceptance. The value of VNG Games is continuously amplified precisely in these seemingly fragmented links that determine a product's lifecycle.

3. Users declined, but revenue still grew: the growth logic is adjusting

Looking at 2025 data, VNG's game business showed a noteworthy change: active user scale declined, but revenue and gross bookings still maintained growth.

According to VNG's 2025 annual report, revenue from Games & Entertainment grew 8% year-on-year, while gross bookings grew 13% year-on-year. At the same time, QAU (Quarterly Active Users) decreased from an average of 74.3 million in 2024 to 57.3 million; the paying-user ratio increased from 3.7% in 2024 to 4.6%.

This set of data should not be simply interpreted as VNG Games having completed some kind of strategic transformation. The decline in quarterly active users may be affected by product cycles, launch cadence, market competition, user-acquisition strategy, fluctuations in casual-game activity, and multiple other factors; the increase in paying-user ratio also needs to be observed together with product mix, core-user retention, monetization events, and operations of mature products.

But it at least points to one direction: the growth logic of VNG's game business may be gradually shifting from simply pursuing a larger user base toward placing greater emphasis on long-lifecycle products, core users, and monetization efficiency.

In 2025, core long-lifecycle products represented by PUBG Mobile and Play Together together contributed **46%** of game-segment revenue.

This shows that mature products remain an important foundation of VNG's game revenue. For publishers, the value of long-lifecycle products is not just stable gross-booking contribution, but also that they continuously validate local operating capabilities: how to organize version updates, how to design holiday events, how to recover churned players, how to manage community sentiment, and how to balance paid content with player acceptance.

Based on disclosed information, VNG also emphasized several directions in 2025 and its outlook: Games-as-a-Service / long-term live-service game operations (a game-service model centered on continuous updates, ongoing operations, and sustained monetization), improved monetization efficiency, prudent launches, platform efficiency, and AI-assisted R&D.

Behind these keywords is essentially the same question: when user dividends no longer expand linearly, competition among game companies is no longer only about "what product they can secure," but about "whether they can keep that product in the market for longer."

Therefore, the user and payment changes in 2025 are better understood as an observation signal rather than a definitive conclusion that has already been realized. In the short term, VNG Games needs to continue proving the operational resilience of its mature products; in the medium term, it needs to improve new-product launch efficiency and retention performance; in the long term, the key will be whether it can build stronger recognizability in global content supply and proprietary content assets.

4. In the competitive landscape, VNG's advantage lies in systematic capability

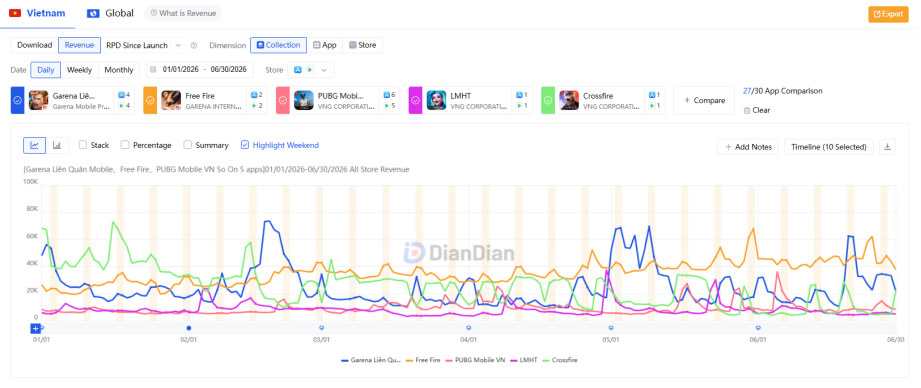

However, VNG is not the only player in Vietnam's game market. To understand VNG Games' position, it also needs to be placed within the competitive landscape.The mostrepresentative reference pointis naturallyaregional competitorfromoverseas—Garena Vietnam. The two companies'core product portfolios overlap significantly: both have long covered long-lifecycle competitive categories such as shooters and MOBAs, and both rely on continuous operations, version updates, esports events, and player communities to extend product lifecycles.

Judging fromproduct revenuecurve performance, Garena's advantages are mainly reflected in two aspects.

First, the revenue curves of its top products are more stable. Free Fire maintained a relatively continuous revenue level throughout the observation period and saw some uplift from May to June. For a shooting game, this stability often means the product still has a strong daily payment base and sustained operating capability.

Second, MOBA products still have the ability to generate periodic spikes. Garena Liên Quân Mobile showed clear revenue peaks at multiple points in time, indicating that around version updates, events, or tournament nodes, it can still mobilize core users to pay. For a long-running competitive product, these peaks are not just short-term revenue fluctuations; they also reflect that the product community and operating cadence remain vibrant.

By contrast, VNG-side products such as PUBG Mobile VN, LMHT, and Crossfire also show several revenue-uplift moments, but their overall curves are more volatile. Some products surged during specific periods, indicating that VNG still has the ability to reactivate players and drive event-related spending; but from a continuity perspective, its representative products were below Garena's two leading products during most periods.

This does not mean that VNG Games is at a disadvantage in competition. More accurately, Garena's advantage is more concentrated in the sustained operation and esports amplification capabilities of single top-tier long-lifecycle competitive products, while VNG's advantage leans more toward the comprehensive capability of a local publishing system.

Backed by the Sea ecosystem, Garena has strong regional publishing experience across multiple Southeast Asian markets and is also better at building tournaments, communities, and cross-market operating rhythms around leading competitive products. The performance of Free Fire and Liên Quân Mobile, to some extent, reflects Garena's maturity in operating regional competitive products.

VNG Games follows a different path. Its core capability is not only whether a single product can outperform Garena, but whether it can plug different types of games into Vietnam's local publishing system: including localization, payments, customer service, communities, events, channels, compliance communication, and potential synergies with group ecosystem assets such as Zalo and ZaloPay.

In other words, if judged from single-product curves, Garena indeed has stronger leadingsamples in the two core competitive categories of shooters and MOBAs; but if judged from company capability structure, the key question for VNG Games is whether it can use a more localized and more systematic operating capability to continuously take on different products and turn a one-time launch into longer-cycle service.

This is also the core difference between VNG and Garena.

Garena is more like a representative of Southeast Asia's regional competitive-product operating capability, with strengths in top products, esports ecosystems, cross-market replication, and community mobilization. VNG Games, by contrast, is more like an infrastructure-type company for Vietnam's local game industry. Its strengths lie in local player relationships, payment understanding, customer service and community operations, compliance experience, and a publishing-service system accumulated over many years.

Therefore, for VNG Games, future competitive pressure will not come only from whether it can produce the next hit, but also from whether it can continue to prove its local operating efficiency and product onboarding capability in the face of regional competitors like Garena.

5. Zalo and ZaloPay are not simply traffic entry points, but tools for player relationships

When discussing VNG Games, Zalo and ZaloPay within the group are easily placed into the same narrative.

Zalo is an important local communications and social product in Vietnam, while ZaloPay provides local digital-payment service capabilities. From a business-synergy perspective, they do provide potential support for VNG's game business: user reach, event recall, customer-service communication, community maintenance, local payment understanding, and lower operating friction.

But this synergy needs to be described carefully. Zalo and ZaloPay are not equivalent to guaranteed growth sources for the game business, nor can they replace product quality, content supply, and the vitality of player communities. Game revenue ultimately still depends on the product itself, version cadence, payment design, user retention, and market competition.

A more accurate statement is that Zalo and ZaloPay form part of VNG Games' capability foundation in local operations.

For example, local social tools can help games conduct event notifications, user recall, and customer-service communication more efficiently; local payment services can improve understanding of players' top-up habits, payment paths, and risk control; and long-accumulated local user relationships can also help publishing teams capture player feedback and market sentiment more quickly.

These capabilities may not directly translate into revenue growth, but they affect the efficiency of game publishing and operations.

For overseas game companies, when entering a regional market, the biggest challenge is often not just user-acquisition cost, but unfamiliarity with local user relationships. Where players discuss games, what events are more readily accepted, how customer-service feedback should be handled, where payment processes may leak users, and which content expressions require localization adjustments—these are not problems that can be solved through advertising alone.

VNG Games' advantage lies precisely in the fact that it does not conduct game publishing in isolation, but operates games within a local digital ecosystem. Services such as Zalo and ZaloPay may not constitute direct traffic dividends, but they can help reduce communication costs, payment friction, and service costs during local publishing and operations.

Such capabilities may not be obvious from the outside, but they often determine whether a product can move from "successful launch" to "sustained operation."

6. The real ceiling still depends on global content assets

If local publishing and long-term operations explain the floor of VNG Games, then global content assets determine its long-term ceiling.

From a business-structure perspective, VNG Games can roughly be divided into three layers: the first is third-party licensed game publishing, which is its long-term revenue foundation; the second is casual game platforms and related studios such as ZingPlay, which provide lighter and more regionalized content supply; the third is self-developed, invested, and co-developed businesses, representing its attempt to extend toward content production.

According to VNG's 2024 annual report, VNGGames has published/launched more than 200 games in Vietnam since 2004 and launched 40+ games in international markets; as of 2024, its game team had more than 1,200 people across nine cities globally; and it launched 17 new games in 2024. In the same year, ZingPlay Game Studios' international revenue exceeded domestic revenue for the first time.

These data points show that VNG Games is no longer just a publishing team serving Vietnam's domestic market, but is continuously expanding its product and team footprint across regional and international markets. The change at ZingPlay Game Studios in particular indicates that its casual-game capabilities are migrating into overseas markets.

However, boundaries also need to be maintained here.

VNG disclosed in its F-1 that in 2020, 2021, 2022, and the first half of 2023, self-developed games contributed roughly around 20% to slightly above 20% of Games revenue. This reporting scope indicates that VNG Games has a certain foundation in content production, but it corresponds to historical years and cannot be directly extrapolated to 2025.

More importantly, an increase in the share of self-developed revenue does not automatically mean that global content assets have matured. It only shows that VNG Games has a certain foundation on the content-production side; going forward, product scale, international user retention, category expansion capability, and sustained overseas performance still need to be observed.

Based on currently disclosed information, VNG Games' internationalization looks more like a combined path of "regional publishing + lightweight self-development + co-development" rather than a content company that has already formed a global blockbuster portfolio.

This is not a negative judgment, but a more accurate description of its current stage. For a company that has long been strong in local publishing and operations, extending toward self-development and internationalization naturally takes time. Publishing capability, operating capability, and local ecosystem capability can help it better take on products, serve players, and improve monetization efficiency; but what truly determines the global ceiling remains the recognizability of original content, cross-market adaptability, and continuous R&D efficiency.

Among VNG's 2026 priorities, it mentioned a stricter launch-evaluation framework, tying capital allocation to engagement and retention thresholds, expanding marketing automation across the full product portfolio, and amplifying ZingPlay Game Studios' validated AI-driven model.

These directions indicate that VNG Games is trying to improve product success rates through more refined evaluation and more efficient production methods.

But the game business is ultimately a results-oriented industry. Evaluation frameworks can reduce trial-and-error costs, AI can improve some R&D and operating efficiency, and platform capabilities can improve reach and service, but what truly keeps players remains the content itself and the ongoing operating experience.

7. For Chinese game companies going global, VNG Games' lesson is not just "find a local publisher"

Returning to the original question: why is VNG Games unavoidable in Vietnam's game industry?

The answer is not only that it has published many games, nor only that it is backed by VNG's local digital ecosystem. More fundamentally, it has long played the role of connector and infrastructure builder in the Vietnamese market.

It connects overseas content with local players, and it also connects game products with payments, customer service, communities, offline events, and long-term operations. Its value is not reflected only in the agency result of a single product, but in a reusable set of localized operating capabilities.

In the short term, VNG Games' core variables are whether mature products can continue supporting revenue and gross-booking growth, and whether new launches can supplement growth momentum. In the medium term, the key is whether it can continue improving monetization efficiency, retention quality, and operating stability amid fluctuations in user scale. In the long term, what truly determines its ceiling remains whether self-developed, co-developed, and international content assets can produce clearer global recognizability.

For Chinese game companies going global, the VNG Games case also offers a reminder: the truly scarce capability of a regional publishing partner is not merely bringing a game into the market, but making the game understood, paid for, served, and operated over the long term locally. For outbound publishers, understanding VNG Games is also understanding what a publisher becomes after a regional game market truly matures.

When entering Vietnam, or any regional market with clear differences in culture, payment, and community structure, the product itself remains the first prerequisite. But beyond the product, who better understands local players, who can better handle payment and customer-service details, who can maintain community relationships, and who can turn one launch into long-term service will often determine how far a product can go.

This is exactly why VNG Games remains worth observing today. It is not a "Vietnamese version of someone else" that can be easily compared, but a type of key company that Vietnam's game industry has gradually formed over the past two decades: starting from publishing and extending into operations, services, platforms, and content production. It may not necessarily have a guaranteed global ceiling, but it has already become one of the most important underlying capabilities in Vietnam's game market.