文

A

Based on comprehensive data from DianDian Data, this analysis integrates the Top 20 mobile game download and revenue rankings for India (App Store + Google Play) in November 2025 (Nov 1–30). It combines core ranking insights with regulatory context, localization trends, and genre dynamics to provide a holistic view of one of the world’s fastest-growing gaming markets.

November marked a strong performance for India’s mobile game market, with both key metrics hitting 2025 highs:

· Total Downloads: Rose 1.66% month-over-month (MoM), driven by casual and niche genres that resonate with India’s price-sensitive and tier-2/3 market users.

· Total Revenue: Climbed 2.51% MoM, reflecting growing in-app purchase (IAP) activity among core gamers and sustained demand for regionalized content.

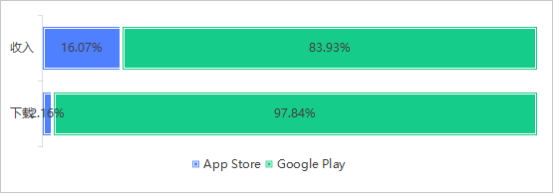

· Platform Dynamics: Google Play maintains an unshakable lead, accounting for over 97.8% of game downloads. While App Store’s market share had previously grown due to Apple’s local supply chain expansion, this upward trend has stalled since August—though its share remains higher than early 2025.

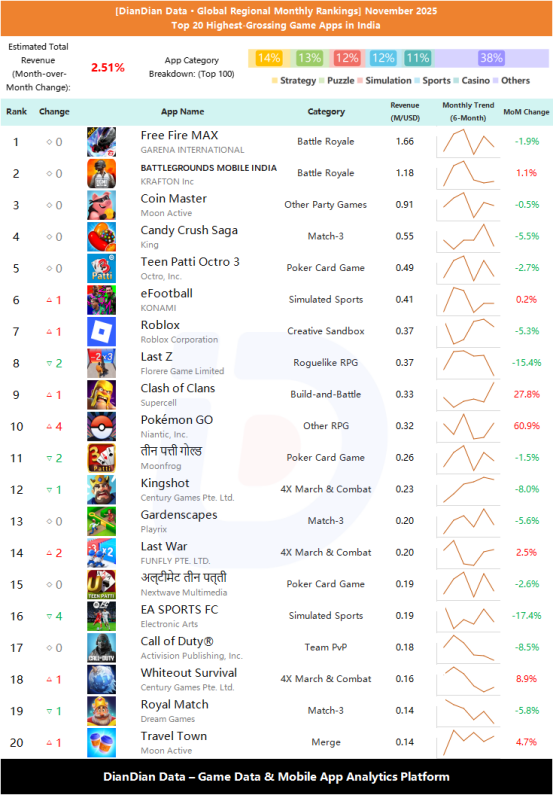

Download Rankings (Top 20): Free Fire MAX Dominates, Real-Money Gaming Makes a Comeback

Top Performers: Battle Royale & Classic Casual Retain Lead

· Free Fire MAX (Battle Royale): Secures the #1 spot with 12.32M downloads (+12.1% MoM), hitting a 2025 peak. Its success stems from Garena’s deep localization efforts—including data partnerships with Indian firms and esports ecosystem rebuilding—since its late-2023 relaunch as Free Fire India.

· Ludo King (Ludo): Holds #2 with 11.96M downloads (-8.2% MoM). Despite a slight dip, the classic board game remains a staple for casual users, especially in rural and family gaming scenarios.

· WinZO Games (Mini Game Collection): Skyrockets 785.6% MoM to #12, a dramatic rebound from its August crash. This resurgence follows high courts issuing interim stays on parts of India’s proposed Online Gaming Promotion and Regulation Bill (which threatened to ban real-money games). To mitigate risk, WinZO shifted from cash contests to “reward points/prize redemption” and emphasized “skill-based competition”—a strategy that resonated with users amid regulatory uncertainty.

· Truck Games (Driving Simulator): Jumps 332.3% MoM to #14, highlighting untapped demand for simulation titles in India’s tier-2/3 markets and rural areas, where vehicle-themed content has strong cultural relevance.

· Top Download Genres: Hyper-casual (27%), Simulation (25%) lead the Top 100, confirming casual’s status as the market’s backbone.

· Rising Subgenres: Endless Runner (e.g., Subway Princess Runner, Subway Surfers) and Driving Simulator (3 titles in Top 20) emerge as breakout niches.

· Action Resurgence: Hunter Assassin (Action) climbs 48.4% MoM, signaling renewed interest in fast-paced, accessible action gameplay.

· Free Fire MAX (Battle Royale): Retains #1 with $1.66M revenue (-1.9% MoM). While downloads soared, flat-to-slightly-down revenue reflects India’s persistent low ARPU (Average Revenue Per User) challenge—even for top titles.

· BATTLEGROUNDS MOBILE INDIA (BGMI) (Battle Royale): Holds #2 with $1.18M revenue (+1.1% MoM), underscoring the genre’s enduring appeal among high-spending core gamers.

· Pokémon GO (Other RPG): Surges 60.9% MoM to #10, marking a massive IAP rebound. The game’s resurgence is likely driven by localized events and increased engagement from India’s growing base of franchise fans.

· Clash of Clans (Build-and-Battle): Rises 27.8% MoM to #9, while Whiteout Survival (4X March & Combat) climbs 8.9% MoM to #18. These gains highlight strategy titles’ ability to drive long-term user retention and spending.

· Poker Card Games: Titles like Teen Patti Octro 3 and तीन पत्ती गोल्ड claim 3 spots in the Top 20, reflecting strong demand for regionalized card game experiences tailored to Indian audiences.

· Key Revenue Genres: Strategy (14%) and Puzzle (13%) lead the Top 100, complementing battle royales to create a diverse revenue landscape.

· Match-3 Stability: Titles like Candy Crush Saga and Gardenscapes maintain steady presence, though most see slight MoM revenue dips—indicating mature but consistent user bases.

1. Regulatory Uncertainty Drives Adaptation: Real-money gaming’s rebound (exemplified by WinZO) shows that platforms can thrive by adjusting business models amid regulatory flux. The interim stays on the proposed bill suggest a likely path to “strict regulation” rather than full bans.

2. Localization = Success: Free Fire MAX’s dual dominance in downloads and revenue proves that deep localization—data compliance, esports, and cultural relevance—is critical for foreign titles in India.

3. Dual-Tier Market Dynamics: Casual genres drive downloads (fueled by tier-2/3 and rural users), while core genres (battle royales, strategy) drive revenue (led by urban, high-spending gamers).

4. ARPU Remains a Challenge: Even top titles like Free Fire MAX struggle to grow revenue despite download surges—highlighting the need for innovative monetization (e.g., hybrid IAP+IAA models) tailored to India’s price-sensitive users.

Want real-time rankings, user behavior analytics, or genre-specific trends for India’s mobile game market? Visit app.diandian.com to explore comprehensive dashboards and data-driven insights for global markets.