文

A

At the beginning of 2026, the Philippine cash loan market will undergo significant changes in regulatory policies. On February 5th, the Philippine Securities and Exchange Commission (SEC) announced 28 unregistered online lending platforms; Subsequently, the draft memorandum of understanding released in March sent a key signal: the four-year ban on platform registration had been lifted, and the industry entry threshold had been significantly raised.

On one hand, there is a heavy handed regulatory crackdown on illegal platforms, while on the other hand, policies are relaxed and compliance thresholds are upgraded. According to DianDian Data's February Top 30 Philippine Lending Apps list, the volatility of the Philippine cash lending industry has intensified, with the user base of cash lending platforms rapidly changing and platforms accelerating their entry or forced exit.

1、 SEC reports 28 illegal lending platforms, with over 140000 active users awaiting diversion

According to DianDian data monitoring, the 28 platforms reported by the SEC in February cover Google Play, Apple App Store, and independent website channels. At present, most of the involved apps have been taken down, but there are still a few platforms that continue to provide services through "covert operations".

In the above list, some illegal platforms have used repeated listings to evade supervision. After USCREDIT's CredLine Online Credit Service was taken down on March 5th, it was re released on March 11th with a new package called Credit Plus Online Loan, but was taken down again just two days later, indicating the complete failure of the "vest tactic".

Among other reported platforms, MII Cash was actually taken down from the app market as early as November 2025, and provided a download portal on the PC side through the "curve saving" method. As of February 2026, its app still has over 10000 active users per month. According to incomplete statistics from DianDian, the cumulative active users of the platforms that have been reported and can be counted have exceeded 140000, including platforms with large user bases such as TalaCredit, Credipillar, and Kuhacash.

Overseas illegal loans and the chaos of "vest bags" are rampant, and the regulatory storm in markets such as the Philippines has put extremely high compliance costs and survival pressure on practitioners. Dian Dian Data has a mature solution for monitoring high-risk/illegal loan applications, relying on real-time monitoring and intelligent analysis of the global application market. By conducting sensitive permission checks, identifying sensitive/zombie comments, verifying developer backgrounds, and scanning privacy policies, we provide comprehensive support for financial overseas enterprises to penetrate regulatory red lines, avoid violation risks, and ensure safe business landing.

2、 SEC strictly investigates four types of violations, and the coordinated supervision of distribution platforms is comprehensively tightened

In February 2026, channels such as Google and Meta joined forces to regulate and increase efforts to clear illegal platforms. At the same time, the requirements for platform listing and access were raised. Multiple factors drove the compliance threshold and purchase cost (CPI/CPA) of the Philippine cash loan market to rise simultaneously.

1. Local supervision and platform collaborative clearance, compliance requirements are rigidly implemented

The SEC continues to push the list of illegal loan applications (OLA) to Google and Meta, and platforms immediately remove the relevant apps and ban associated advertising accounts upon receiving them.

Mandatory Disclosure: All advertisements and app interfaces must prominently display the SEC registration number and CA number.

Data compliance: The platform needs to connect to the National Credit Center (CIC) to submit borrower data in order to reduce the risk of multi head lending.

2. SEC rigorously investigates four types of violations, accelerating market structure adjustment

The focus of regulatory inspections is on the following four types of violations:

Unlicensed operations, shell companies, or illegal use of sub contractors for advertising;

Using gimmicks such as "zero interest rates" for misleading promotion;

Mandatory acquisition of mobile phone permissions unrelated to credit;

Core information such as repayment period, annualized interest rate (APR), and total loan cost have not been disclosed.

3. Google: Financial service verification landing, skyrocketing traffic costs

Google has included the Philippines in the financial services verification market, with a verification deadline of April 14, 2026. Starting from March 10th, compliance partner G2 will handle applications, and advertisers must hold a CA lending qualification issued by the SEC in order to advertise.

February is at the end of the grace period, and some unlicensed accounts are competing for volume, further driving up traffic competition and advertising costs.

4. Meta: Double tightening of advertising and payment, continuous increase in customer acquisition costs

Advertising control: Loan advertisements are classified as a special category and are prohibited from targeted targeting specific audiences, resulting in a passive decrease in Customer Acquisition Efficiency (CPA).

Cost overlay: Facebook ads are subject to a 12% value-added tax and are fully transmitted to the advertising terminals, further increasing customer acquisition costs.

Under the tightening regulatory situation mentioned above, the number of newly launched cash loan applications continues to decline. According to DianDian data monitoring, there were 62 cash loan applications launched in the Philippines in January, which decreased to 54 in February. At the same time, driven by the huge demand from users, lending assistance tools such as accounting management and credit management have gained certain growth potential.

3、 TOP30 list: Home Credit Philippines' growth rate declines, Mr. Cash's dual growth catches up, Big Loan banned for illegal related party transactions

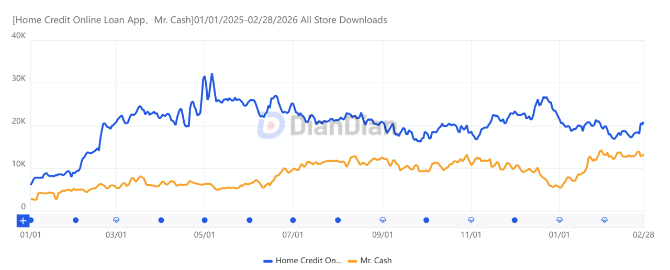

According to DianDian data, in the top 30 lending apps in the Philippines in February, Home Credit Philippines led the industry with 1.378 million monthly active users, but slightly decreased by 4.49% compared to the previous month; Mr. Cash ranked second with 745000 monthly active users, a month on month increase of 11.54%; MabilisCash, Tala, and JuanHand rank third to fifth respectively, with monthly active users exceeding 500000.

Interpretation of Core Data in the Ranking:

Home Credit Philippines, a subsidiary of Jiexin, ranks first in the Philippine market with 1.378 million monthly active users, but both monthly active users and downloads have declined, and its growth momentum has weakened. Mr. Cash, as the second ranked platform in the industry, has shown strong performance, with both monthly activity and download volume increasing. It is the only platform in the TOP5 that has achieved dual growth, and its growth momentum is very prominent.

In the Philippine cash loan market, platform performance is significantly differentiated and risk is intertwined. Some platforms have seen a surge in short-term users and download data, while others have been taken down due to compliance issues. As LoadCash's monthly live sales surged by 214.63% and downloads increased by 21.16%, it entered the 26th place on the list; PeraMoo's download volume surged by 33.97%, with a significant increase in customer acquisition, ranking 13th. At the same time, traditional top platforms such as MabilisCash, Tala, and FT Lending have seen a synchronous decline in monthly activity and download volume, further reflecting the extremely unstable situation of the Philippine cash loan market platform and the rapid migration of loan users.

The Big Loan product belongs to Fingertip Finance Corp., with Philippine SEC compliance registration number 2020070001053-00 and authorization certificate (CA) number 1319. It is qualified and compliant, but it was involved in a major regulatory action against Digido Lending in March 2026.

Due to its involvement in assisting the disqualified entity Digido to continue illegal operations, Big Loan under Fingertip has been delisted from Google Play for compliance in response to the SEC's crackdown on illegal financial chains.

According to DianDian data monitoring, the Big Loan platform has a monthly active user base of over 100000, ranking 27th among the top 30 platforms. In February, the monthly active users increased by 15.67% and the download volume increased by 23.62%. The growth momentum was relatively strong, but after being investigated and reported by regulators, it was taken down from the Google Play Store on March 24th.

Before being taken down by the store, according to DianDian data monitoring, a large amount of sensitive information related to the normal operation of the platform, such as "unresponsive applications", "unable to apply for loans", "unable to log in and repay", had emerged on the user side, and it is still increasing. Dian Dian Data provides a high-risk/illegal loan application monitoring solution, covering sensitive permission screening, sensitive/zombie comment recognition, developer background verification, and privacy policy scanning. It provides long-term and timely risk insight services such as industry changes and violation warnings for regulatory agencies and industry practitioners.

4、 SEC policy shift: ban lifted, threshold significantly raised

On March 12, 2026, the Securities and Exchange Commission (SEC) of the Philippines officially released a draft memorandum circular on lifting the ban on online lending platforms (OLPs) and establishing requirements for prudence, disclosure, and market conduct, soliciting public opinions.

This draft sends two key policy signals. One is to end the registration ban implemented since November 2021, and the new platform can reapply for registration. The second is to significantly increase the entry threshold, and the new regulations will directly link the paid in capital with the number of operating apps.

According to the new regulations, a loan company operating one online loan platform needs to pay 20 million pesos, operating 2-5 platforms requires 30 million pesos, and operating 6-10 platforms requires 50 million pesos; The financing company needs to pay 30 million pesos to operate one platform, 60 million pesos to operate 2-5 platforms, and 100 million pesos to operate 10 platforms. Existing companies can enjoy a 3-year transition period to replenish their capital.

The new regulations also strengthen consumer protection and clarify three major prohibitions: it is strictly prohibited to obtain the borrower's contact list, social media friends, or SMS records; Prohibit automated collection SMS and any form of harassing collection; It is prohibited to outsource core lending functions. This means that gray methods such as violent debt collection and privacy threats that the industry has long relied on will be completely banned.

Summary

The Philippine cash loan market is at a critical crossroads: on the one hand, regulators are cracking down on illegal platforms, with over 140000 active users waiting to be redistributed; On the other hand, the lifting of the registration ban has significantly increased the entry threshold, accelerating the survival of the fittest in the industry.

What kind of changes will the Philippine cash loan market face in the next three months as the SEC's new regulations deepen their implementation? Pay attention to DianDian data and keep up with the latest overseas market trends.