文

A

In the fourth quarter of 2025, the online consumer market in Mexico will perform strongly. Stimulated by shopping festivals such as El Buen Fin, retail sales in November increased by 4.4% year-on-year, setting a two-year high. In December, the Mexican central bank significantly lowered its benchmark interest rate by 100 basis points to 7.0%, further reducing credit costs and helping with economic recovery. Multiple factors such as the decrease in credit costs and the resonance of holiday consumption demand have driven the consumer confidence index back to 44.7, reversing the previous downward trend.

The Mexican cash loan market is experiencing sluggish growth, with quarterly cumulative downloads decreasing by 5.45% compared to the previous quarter

Contrary to the rebound in the consumer market, the Mexican Cash Loan market showed signs of fatigue in growth this quarter. According to DianDian data monitoring, the quarterly download volume of lending apps in Mexico ended two consecutive quarters of positive growth in the fourth quarter of 2025, falling back to 29.2903 million times, a decrease of 5.45% compared to the previous quarter.

DianDian data analysis suggests that the decline in the download volume of lending instruments in the region is not a random market fluctuation, but rather stems from the seasonal characteristics of the Mexican credit consumption market, which are influenced by the following factors:

1. Substitution effect of payment tools: In year-end promotional activities such as "El Buen Fin", traditional banks represented by Banamex, as well as BNPL tools such as Kueski Pay and Aplazo, have deeply integrated with local mainstream e-commerce platforms such as Amazon and SHEIN, providing up to 10% -30% cashback on bills and ultra long interest free installment plans, significantly diluting the download volume and activity of cash loan apps with relatively high daily interest rates.

2. Short term liquidity is sufficient due to statutory benefits: According to Article 87 of Mexico's Federal Labor Law, employers must distribute Aguinaldo (year-end double pay) to all regular employees before December 20th. This system enables the personal cash flow of the public to reach its annual peak at the end of the year. For many low - and middle-income families, Aguinaldo has become an important source of funding for year-end expenses, debt repayment, or holiday purchases, temporarily reducing the short-term demand for high-frequency, small-scale emergency loans.

3. The impact of strategic contraction in supply side risk control: In December, Mexican banking institutions significantly strengthened their prudent provisioning strategy for low-income groups and non collateralized credit loans, by raising approval thresholds to prevent default risks that may arise from year-end consumption impulses. Cash lending platforms are no exception. Faced with the potential increase in bad debt risks at the end of the year, most platforms proactively shift their focus from acquiring new users (CAC) to managing existing users and ensuring risk protection, in order to maintain a stable non-performing loan ratio (NPL) in their annual reports.

Mexican cash lending platforms are experiencing intensified volatility, with DiDi Finanzas being delisted for 14 days and MexiCash and Fortaprest experiencing a decline in both activity and downloads

2025年第四季度,墨西哥数字信贷市场各应用的月活跃用户(MAU)与下载量环比变化剧烈。其中,《DiDi Finanzas》以367.5万的月均活跃用户数遥遥领先,其在Q4活跃用户环比正增长的同时,下载量环比下降11.97%;《Aplazo》、《Credmex》等紧随其后,呈现相似态势。相反,例如《App Crédito Fonacot》的下载量环比激增159.44%,月活骤降22.21%,显示出当地市场高度波动与动态竞争的现状。

Didi's third quarter financial report released in November 2025 showed that its total global transaction volume (GTV) in international business reached 29.8 billion yuan, a significant increase of 31% year-on-year, far exceeding the growth rate of 10.1% in domestic business. Although the sector still has an adjusted loss of approximately RMB 1.7 billion, it remains a certain growth engine for the company. Data shows that as of December 2025, Didi's digital financial service users in Latin America have exceeded 25 million. DiDi Finanzas, as a credit and payment tool for drivers and passengers, achieved an average of 3.675 million monthly active users in the fourth quarter of Mexico, a year-on-year increase of 8.82%, demonstrating strong user stickiness.

According to DianDian data monitoring, DiDi Finanzas has consistently performed well in the financial (free) rankings of the Mexican App Store, with rankings mostly between 5-15. However, on September 21, 2025, its ranking rapidly soared to first place, followed by a 14 day store review and delisting. Due to the cold download of lending tools in the current season, its market ranking has been fluctuating and declining since October 6th.

【 DianDian Data 】 Long term provision of App market share analysis, store diagnosis, and ASO optimization strategy services. From the perspective of potentially triggering application market management rules, DiDi Finanzas' situation this time is in line with Apple's review logic for manipulating rankings:

1. Alarm triggered by abnormal data: DiDi Finanzas ranking deviates from the long-term trend and "rises vertically" in the short term, which will immediately trigger the monitoring of Apple's anti fraud system. For example, if the overall application ranking rapidly rises from outside the 80th place to 8th place within a day, and the financial ranking rapidly rises to 1st place, it may be judged as suspicious non organic growth.

2. The most likely trigger: This instantaneous peak is usually related to short-term strong motivational activities. Didi has increased its marketing and user incentive efforts in Mexico in the second half of the year, such as "extra cashback" or "limited time interest free/fee reduction" promotion activities, which could easily constitute Apple's ban on "induced downloads" and lead to abnormal concentration of download data in time and space.

3. Subsequent impact: Clearing the list will affect the natural traffic of DiDi Finanzas' store rankings. After the clearing period ended, coupled with the lack of natural growth after the incentive activities ended, the search ranking continued to fluctuate and decline, which is consistent with the monitoring trend of DianDian data. For example, DiDi Finanzas fell to 20th place in the subsequent application finance ranking in November, and the application overall ranking fell to 161st place in the second half of December.

As the market returns to normalcy, DiDi Finanzas has regained its dominant position, with its financial ranking rapidly rising to an average of 10.2 in the last month of this quarter, while Aplazo's ranking for the same period has declined to 27.8. This reverse fluctuation validates users' inherent preferences for top tier applications and the zero sum nature of market competition among similar customer groups.

In the Mexico region, the Google Play Store is the traffic driven channel and the main battlefield for major cash lending and BNPL platforms to acquire new users. In the fourth quarter, although "Aplazo" performed well on the App Store chart, its iOS download volume increased from 76700 in the third quarter to 92100, an increase of about 20.2%, which is directly related to its rise in Apple's financial ranking. However, the download volume of "Aplazo" on the Google Play Store in the fourth quarter of 2025 decreased from 491000 in the third quarter to 388000, which completely offset the growth of iOS and led to a 15.4% month on month decrease in its total download volume in the fourth quarter. This highlights the dominant influence of the Google Play Store as the main download channel for Mexican lending apps.

Credmex, a subsidiary of Fintopia Group, maintained a stable average active ranking in the Mexico region this quarter, maintaining its third place in the market. However, its Q4 download volume has experienced a significant decline, with a scale of 1.077 million times, a month on month decrease of 26.42%. Daily active users have a certain lag and also show a downward trend.

DianDian Data Analysis believes that the fourth quarter is a peak period for e-commerce giants' buying volume, and the soaring cost of traffic (CPM) will lead to a significant increase in customer acquisition cost (CAC) for cash lending platforms. If we continue to increase investment in the app store at this time, it is not conducive to cost and risk control, so "retention" is more important than pursuing "download growth" (customer acquisition speed).

Changes in download volume of Credmex across all stores in Mexico from May 1, 2025 to May 12, 2025

Daily activity changes of Credmex in all stores in Mexico from May 1, 2023 to May 12, 2023

In terms of other platforms, Tala's average monthly active users reached 953000 in the fourth quarter of 2025, a month on month increase of 7.51%, with a download volume of 1.679 million times, a slight decline; However, platforms such as MexiCash under KuaiNiu Intelligence and Fortaprest under Lexin have experienced varying degrees of decline in monthly active users and cumulative downloads. DianDian data analysis suggests that the deviation between short-term active growth and download trends reflects the prudence of the company's dynamic operations; If both decrease simultaneously, caution should be exercised.

Other developments in the Mexican market: accelerated license consolidation, high interest deposit taking nearing completion, transparency of borrowing costs

In September 2025, Klar reached an equity purchase agreement with Banorte, the largest local bank in Mexico, to fully acquire all shares of its digital bank Bineo. By acquiring Bineo, Klar can directly inherit the formal banking license that Banorte has applied for and holds for Bineo, thereby freeing itself from the business restrictions imposed by relying solely on "crowdfunding" or "electronic payment" licenses (such as deposit limits). On December 8th, the Mexican National Antitrust Commission (CNA) officially approved the transaction, stating that it would not have a negative impact on market competition.

Although Bineo is the first pure digital bank in Mexico to obtain a formal banking license, it has faced profit pressure within less than two years of its launch. According to the financial report, Bineo incurred a loss of approximately $12 million in the first half of 2025, making it the only loss making subsidiary under Banorte. It is reported that Klar plans to use its scaled online user base to offset Bineo's operating losses and launch new business units such as "Klar Empresarial" using Bineo's license structure.

https://thepaypers.com/mergers-aquisitions-and-investments/news/klar-acquires-digital-bank-bineo

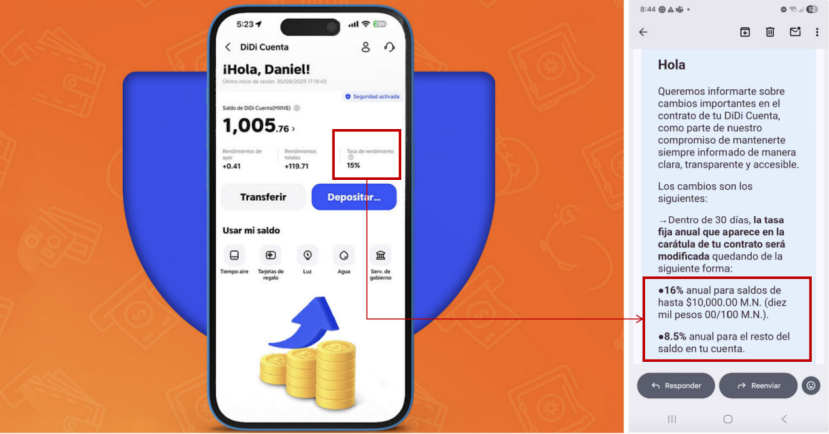

In October 2025, DiDi Pay/DiDi Cuenta sent an email notification to Mexican users announcing significant adjustments to its high interest savings product rules starting from November 2025. Previously, Didi quickly became popular in the local market with its aggressive strategy of 15% annualized returns, no investment threshold, and funds available on demand, but this undoubtedly brought a heavy interest burden to the platform. After adjustment, Didi Financial's deposit products will enjoy a 16% yield within the set limit (10000 pesos, approximately RMB 4000), and the excess will be calculated at 8.5%.

DianDian Data Analysis believes that the logic behind Didi Financial's new regulations is to use the leverage of tiered interest rates to leverage the maximum brand effect with the lowest interest expenses, thereby improving EBITA profits in the fourth quarter and achieving a transition from extensive customer acquisition to refined cost control. This plan is highly attractive to groups with limited idle funds in the ecosystem such as drivers and food delivery drivers, and also helps to achieve "ecological feedback finance". Against the backdrop of the Mexican central bank's continuous interest rate cuts, the high interest dividend will gradually narrow, and in the future, "flexibility" may become a more important competitive dimension than "pure interest rates".

In November 2025, the Bank of Mexico (Banxico) officially released a draft for soliciting opinions on revising its Circular 21/2009, which explicitly requires all credit related fees, interest, commissions, and additional expenses to be included in the CAT (Total Annualized Cost) calculation to prevent institutions from splitting some fee items outside of the total cost.

The core objective of this draft is to redefine the calculation methods and disclosure rules of CAT, aiming to enhance financial market competition and protect consumers through "transparency of borrowing costs". Banxico expects to officially implement the revised rules in early 2026, by which time all licensed financial institutions in Mexico (including fintech entities such as SOFOM and IFPE) must synchronously update their billing systems.

https://mexicobusiness.news/finance/news/banxico-seeks-input-new-cat-rules-boost-transparency

DianDian Data (https://app.diandian.com/?utm_lan=en) is a leading global provider of mobile app and gaming market intelligence, covering 276 countries and regions with real-time monitoring across the top 8 app distribution platforms. Leveraging our high-caliber data infrastructure, we deliver comprehensive, reliable decision-support tools to mobile developers, publishers, fintech enterprises, listed companies, and investment institutions—encompassing key metrics such as app downloads, revenue, user behavior, competitor performance, and SDK integration data. We also provide specialized growth services focused on App Store Optimization (ASO) and Apple Search Ads (ASA). Our solutions empower businesses to pinpoint growth opportunities and accelerate performance in the highly competitive global mobile market.